The Last Down Payment You'll Ever Pay

From Then On, Your Fixed Up Properties Will Cough Up

The Dough For Future Down Payments

If you’ll follow my script for buying income-producing properties, the last down payment you’ll ever have to pay from your own wallet will be for the first property you purchase. Allow me to repeat that! You should never need to pay another down payment for subsequent properties from your personal funds if you’ll purchase the kind of properties I recommend! I’m talking about the rundown fixer-type properties. For each new property you acquire, the down payment will be funded by the added value you’ve created on the property before. This strategy was taught to me early on by my mentor William Nickerson. Bill called it the 3 R’s: Repair, Renovate and Refinance.

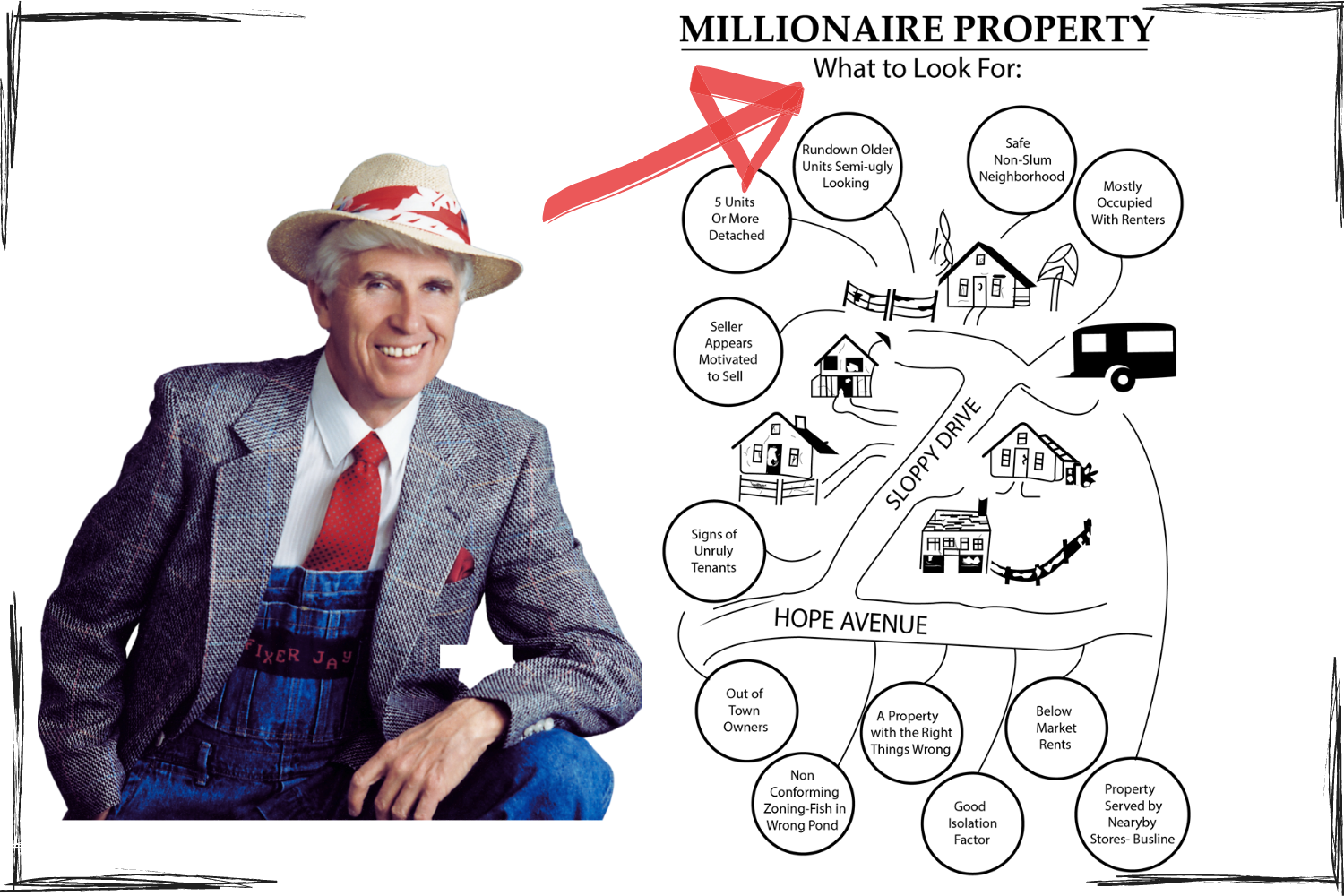

My investment goal is to purchase rundown multiple unit properties at a discounted price because of their condition and lack of upkeep. My target properties range in size from 5 to 12 units.

The value of these properties are pretty much determined by how much income they generate. Rundown properties commonly rent for less and stay vacant for longer periods of time. As a result, these properties have less value to potential buyers and must be discounted if sellers are serious about selling.

From an economic standpoint, an owner like myself can repair and renovate these properties for roughly one-tenth the cost of replacement. For new investors willing to jump in and provide “non-technical” labor themselves, the cost difference between fix-up and replacement will likely be a lot more. Fixing up the property and increasing the income to top market rates is the fastest method to create large equities and substantial cash flow. If you can pull this off, there’s no doubt in my mind, you’ll soon join the millionaires who are doing this as I write.

LARGE EQUITIES ARE LIKE MONEY IN THE BANK

I’ve already promised you, your first down payment will be the last one you’ll ever pay! I mean you personally will ever pay. From now on your fixed up property is gonna cough up the dough! In the very first sentence I told you: “If you’ll follow my script!” A major part of my script is to purchase rundown, often ugly-lookin’ properties that very few buyers want. As you can probably figure out, the sellers of these kinds of properties have far fewer opportunities to sell. This means they must be a lot more flexible if they truly wish to sell. Flexibility means selling cheaper! This is how I build equity quickly for my next down payment. Let’s take a look at how this happens!

Say for example I purchased a rundown property for $300,000. The seller accepted my 10% cash down payment ($30,000). Next, I will jump in and apply the 3 R formula – Repair, Renovate and Refinance. I’ll attempt to skip the refinance if I can. After my fix-up, repairs and increased rents, I now own a property worth $500,000. By the way, this is a very reasonable value increase. I have often doubled the property value in two years or so.

.png)

In this example, I purchased the property for $300,000 with a $30,000 cash down payment. The seller has agreed to carry back a private mortgage ($270,000) for the balance with payments for 20 years. My increased equity after fix-up is approximately $230,000. I’m now ready to begin my search for the next fixer-upper property. This time I plan on using my newly created equity for the down payment instead of my personal cash. There are basically two fairly common methods I can use to accomplish this.

The first method – my preferred method is to create a 2nd note or mortgage secured by my newly fixed up property and use it for my down payment.

.png)

This method will require a somewhat motivated seller. I’m talking about a seller who would rather have a secure mortgage with monthly payments coming in instead of the rundown property he now owns. When negotiating, if he sounds interested, I’ll start working out the terms. For example, let’s say I offer $40,000 down payment in the form of a secured note. My typical offer today might be a $40,000 note for 10 years with amortized monthly payments of $444.09 at 06% interest. I always explain to the seller: If you accept my offer, you’ll actually be receiving over $53,000 for your down payment.

The paperwork is easy enough to do yourself. You simply need a blank deed of trust and promissory note in my state (California). A mortgage in many other states. Fill in your negotiated terms. Deed signatures must be notarized, same for mortgages. The county recorder can show you the paperwork needed for recording. Using the example above, after recording, I would now have a 1st mortgage of $270,000 and a 2nd mortgage of $40,000 on my newly fixed up property. The equity cushion or safety margin securing the seller’s down payment note would be $190,000 equity or 62% LTV (loan to value). That’s considered very safe.

In the paragraph above, I told you method one was my favorite method for paying the down payment. There are several reasons, but let me tell you the most important. In nearly 50% of the cases, I have purchased my down payment – mortgage back for substantially less than the balance owing. How in the world can you do that, you ask? For the same reason I was able to purchase the seller’s rundown property in the first place. Sellers who can’t manage their property and the tenants are poor managers. They can’t manage their money any better. They’ll always be broke and they’ll always need money. In one case I only paid $13,500 cash to buy back my $30,000 note with a $27,000 remaining balance.

Method Two works well when the seller demands all cash for his down payment and you’re very determined to buy his property.

.png)

This time I’ll turn to a third party for help! A hard money lender. These folks are equity lenders. Borrowing money on my fixed-up property is fairly easy. Using the example above – the seller has agreed to take a $40,000 down payment, but he insists on all cash. As a general rule I can borrow $40,000 on my fixed-up property – no problem once the lender determines I have enough income (rents) to support both mortgage payments. I expect the hard money loan to be for a term of 5 years (max), and the payments and interest will be a bit higher. I’ll give the loan proceeds to the property seller for his cash down payment. In this example the LTV ratio is 62%, same as it was when I created a mortgage for the down payment.

Every once in a while I’ll run into a “hard-nosed”, by the book hard money lender who won’t make a loan when both mortgages exceed 60% LTV. In the case above, (62%) will likely not be approved. Here’s a remedy that will generally soften up the lender. Write the loan for $50,000 instead of $40,000. The lender will only fund the loan for $40,000. The extra $10,000 will be the discount or lender bonus. Sure, you’ll be paying back $50,000 in order to get your $40,000 cash down payment, but you’ve accomplished the task. The object here is to keep the line moving without opening your wallet!