Seller Financing Designed For Profits

The most profitable pillar supporting my real estate wealth!

RENT INCREASES ALL MINE TO KEEP

Seller carryback financing has been one of the most profitable pillars supporting my real estate wealth. I’m talkin’ about buying the kind of income properties where the seller agrees to finance or carry back a note (mortgage) for a big percentage of the selling price – or at least the seller’s equity portion. You can read a great deal more about seller financing in my best-selling books, (available at bookstores or Amazon), but for now, I want you to understand a few basics about the design or “setting up” private financing to maximize future benefits long after the sale is over and done with.

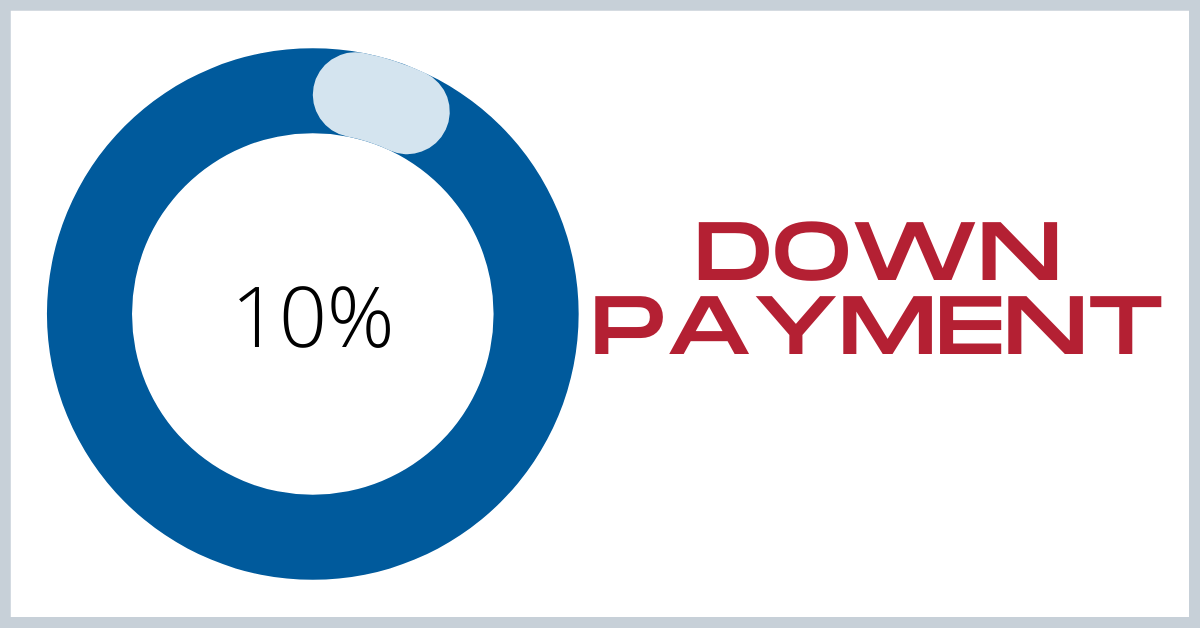

A typical buying situation for me involves dealing with a seller who wishes to sell his property, but for whatever reason, his property won’t qualify for regular bank financing. The most common reason is the property is over 4 units – older and rundown. That’s my target property. With this type of property, the seller is almost forced to provide financing – or at least a good part of it. Quite often I’ll assume or take over an existing mortgage (subject to). In this case I’ll likely pay a 10% down payment – take over the existing mortgage and set up seller financing for the balance (his equity).

Almost every seller I’ve dealt with wants a bigger down payment. Regardless, 10% is my average payment, although I’ve occasionally paid 20%. The reason 10% normally works is because the seller has allowed his property to run down, which greatly limits potential buyers. Sometimes I’m the only buyer to write an offer. This means I have the upper hand during negotiations. In case you’re wondering why sellers want a larger down payment! The answer, they’re usually broke or very close to it. These kinds of sellers will always need money – they can’t manage property or their money.

When you purchase a property using a title company or escrow office which is common in trust deed states like mine (California), you must provide the terms you wish to have included in the note. For the purpose of this blog, a note or mortgage is synonymous. In mortgage states, attorneys will likely prepare the closing papers (escrow). But regardless, you must have an input in the preparation to make sure the terms you want are written in the note or mortgage. Specific terms are needed to give you flexibility or the legal rights to maneuver.

An example of a term you don’t want with private or seller carryback financing is a due-on-sale clause. This clause means if you sell, transfer or alienate the property, the note or mortgage must be paid off in full. This clause is automatically written into every bank or institutional note or mortgage. With seller financing you can avoid it by providing a list of clauses you wish to have drafted into your loan documents to whoever prepares the note or mortgage. If you don’t participate, most escrow officers and/or attorneys will simply draw up standard terms. Obviously, sellers must be in agreement with the terms as well, however; I’ve found that most motivated sellers rarely quibble over terms. Their primary concern is mostly about closing escrow and getting their hands on the money.

The first right of refusal is a term you do want. It means the note or mortgage holder, the person who sold you the property, must come to you first if he or she decides to sell the note or mortgage. Usually, the seller carryback notes I negotiate and help design are very weak. They are not very marketable to professional note buyers (brokers). They have long-term paybacks (20 years), low interest rates and they lack the protective terms most note buyers require. They also lack adequate security because of my small 10% down payments. Professional note buyers usually insist on a 20% equity cushion between the property purchase price and the face value of the carryback note. Even if a professional buyer should offer to purchase the note, their discounted offer would likely upset the seller so much that he or she would stomp out of his office calling him some very disrespectful names. By having a FIRST RIGHT OF REFUSAL CLAUSE in my notes, the note holder must give me the first opportunity to purchase the note. Naturally, I’m very much aware of the discounted value as well. I’ll generally pay a few dollars more than a note broker to avoid the name calling!

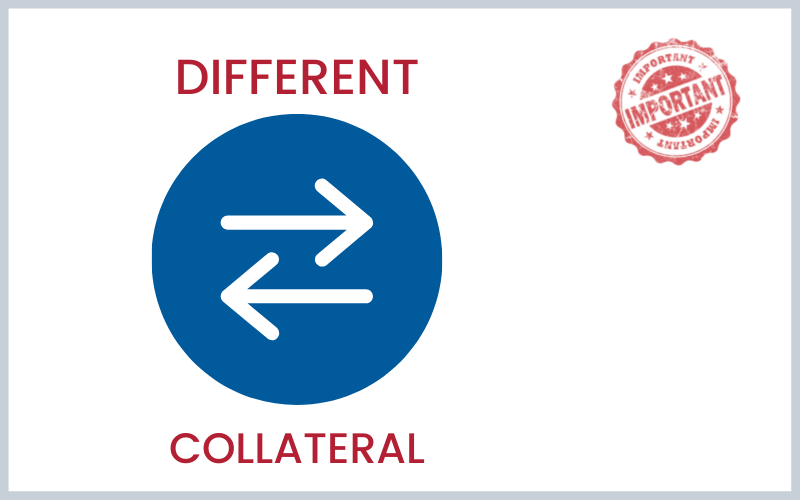

Substitution of collateral is another important clause I wish to negotiate in my notes. Here again, the seller of the property must agree with me, but as I told you before, most sellers I deal with are always in a hurry to close. Their primary goal is getting the money. I’ve had very few sellers put up a fight over terms or clauses I ask for. With several who balked, I added a few dollars to the down payment and their resistance melted. With a substitution of collateral clause, you can transfer the note or mortgage to another property of equal or greater value. A substitution clause allows you to move the seller’s note from the property you just acquired to another property you own. Your other property now becomes the security for the seller’s note leaving your latest purchase free of debt. You can now borrow cash money using the mortgage free property as security. Transferring the seller carryback mortgage to another property is often called: “Walkin’ the Mortgage”.

All banks or institutional notes (mortgages) will contain a late fee clause and most likely an acceleration clause. A late fee is an added charge to the borrower or note holder if the monthly payment is more than 10 days late. When I design private seller carryback notes, I’ll always leave out the late fee clause unless the seller objects. Without a late fee clause, professional note buyers will discount the purchase even more, if indeed, they are interested at all. As I mentioned before, a note without protective clauses or the opportunity to earn additional fees weakens the note, thereby reducing its value to a note buyer. If the property seller should catch my omission, I’ll add it back in. No harm – no foul!

An acceleration clause works pretty much the same as a due-on-sale clause except it’s a bit broader in terms of what it covers. Obviously it’s triggered by a sale or transfer of ownership same as a due-on-sale clause, but it also covers other events that jeopardize the security of the note, such as destruction of the property, often referred to as waste. Removing a building or allowing the property to rundown, thereby reducing the value backing the note or mortgage would likely be grounds for acceleration - meaning the full unpaid balance of the note becomes immediately due and payable. I once owned a property financed by a seller who insisted on an acceleration clause stating; if I didn’t grade the dirt entrance road annually, he would be allowed to accelerate the full payment of his note immediately. ENFORCEABLE; I’m not sure! But I kept the road in good condition so the clause didn’t bother me. Leave this clause out of your seller carryback notes if you can. Can ya say Amen!