Financing Is The Key To Real Estate Wealth

Older, rundown properties are my specialty. I consider seller financing to be a tremendous benefit when buying. I can make the terms and decide the payments.

For those who have read my books, you already know my favorite kind of real estate financing is private financing or as I call it seller financing. Granted, seller financing is not typically used for buying homes or single family houses. However, it’s quite common for investors who acquire 5 or more rental units in a group.

As most readers know, older rundown properties are my specialty. I consider seller financing to be a major benefit. It’s one of the biggest reasons I purchase multiple unit properties to begin with. Investing is about income and profits and as you shall see, private financing provides an opportunity to accelerate both.

Real estate investing is a people business. The late Warren Harding, investor and seminar instructor, always told his students: “You don’t dance with real estate, you dance with the people.” As a long time investor, I can tell you that many decent properties can be found in the market place, but the right terms must be negotiated to produce a money-maker – people dealing with people! Financing is the “heart ‘n soul” of investing. Financing has everything to do with profits and cash flow. Financing, by itself, can turn a great looking property into a total nightmare and a rundown property into a goldmine.

Most investors like myself start out with a very small bank account. This means buying properties for cash was out of the question! I’ve always felt fortunate when a seller would accept 10-15% cash down and allow me to pay off the balance over time. Allow me to interrupt myself here to say I’m not opposed to paying cash for a property, but I rarely run into a newbie who has much cash, so for now I’ll just assume you’re starting out the same way I did.

When you only pay only 10% down for a property, you still owe the seller 90%. The mortgage payment will most always be your biggest monthly expense. Sometimes it’s too big.

For residential income properties, a mortgage payment that requires more than 60% of the rental income is flirting with danger in my opinion. 50% is my target. This brings us to the first reason why seller financing is so important to me. It gives me the opportunity to negotiate my monthly mortgage payments with the seller. Obviously, banks or institutional lenders don’t negotiate payments. They determine the payment and that’s it! The only way you get what you want is to negotiate with real people.

Negotiating seller financing is like fighting for your survival in the wild west. Hardly any restrictions apply and the rules can be pretty much what both parties agree to! Quite often the personal needs of the seller will influence the outcome. For example; if the seller’s unruly tenants are driving him bonkers, there’s a real chance he’ll seriously consider my request for lower mortgage payments – he wants out! The greater the seller’s motivation – the more concessions he’s likely to give me. This is why I purchase rundown and often troublesome properties to begin with. When I sense the seller has problems, it gives me the upper hand with negotiations.

My number one investment goal is cash flow.

Cash flow is the difference between surviving or going broke. Mortgage payments have everything to do with cash flow – or the lack of! For example, amortized mortgage payments suck a great deal of the monthly income from rental properties. There’s no law that says mortgage payments must be amortized. Only the banks say so. Let’s say I was paying off a $300,000 mortgage to the bank – amortized for 20 years at 6.0% interest, my payments would be $2,149 per month. On the other hand, with seller financing, let’s say I could negotiate interest only payments of 6.0% on the same $300,000 mortgage – my payments would only be $1500 per month. The property would now produce $649 additional cash flow.

One of the most profitable strategies for me happens after I’ve already purchased a property and negotiated a private mortgage with the seller. Down the road there’s an excellent chance I’ll have an opportunity to buy back my mortgage for a substantial discount! You might be thinking to yourself; why in the world would the property seller allow Jay to buy back his mortgage for less money than what he owes? There are many reasons, but once again, personal needs come into play. The kind of sellers I deal with are generally poor property managers and most always poor money managers as well! It’s my guess; he’s probably broke and needs money. I’ve found that property owners who sell me their rundown troubled properties are generally broke soon after the sale. It’s been my experience these poor money managers will always need more money.

Let’s say it’s down the road now and the seller calls me! Jay, he says; I realize it’s only been about a year since you purchased my property and I thank you so much for your prompt payments every month – but here’s the deal Jay; I’m in a real tight spot right now and I really need the cash! Is there any way you could pay off your $300,000 mortgage now? Oh boy, Mr. Seller, I’d love to pay you off, but I don’t have any money right now - how long can you wait?

Jay, I’ve already tried to sell my note to a professional note buyer, but since you only paid 10% down, he told me there’s not enough equity in the property! Also, the note needs a bit more seasoning he says; you’ve only been receiving payments for a year or so. He advised me to come back and see him in another 12 months. Jay, there’s no way I can wait for 12 months! Is there any way you can help me here? Well Mr. Seller, I just don’t know! I can call my brother in Chicago, he sometimes buys secured notes!

Ring, Ring, Ring: Hi Mr. Seller, it’s Jay here. I just heard back from my brother in Chicago. I’ve got some good news – and maybe a little bit of bad! He’d love to buy your note, but he only has $150,000 cash saved up right now! If you could somehow make that work, he could get you the money by Friday. Friends, I can promise you this; if the seller is as motivated as he sounds, there’s an excellent chance he’ll take this deal. By the way – a small confession is in order here. I don’t have a brother in Chicago! But guess what! The seller couldn’t care less!

After paying $330,000 for the property – with 10% or $30,000 down and a seller carry-back mortgage for $300,000, I was quite satisfied with the deal. During my negotiations with the seller, he did everything possible to convince me he was selling a smooth running property. However, I had done my own research and discovered an unreported vacancy and two tenants who were several months behind with their rents. It was clear; he was selling me his tenant problems. Long story short – he wanted out and I knew it. Even so, I felt the property was a real bargain from the beginning. I was very happy to negotiate the deal.

Obviously, no one can predict with any certainty whether a seller will come back asking for cash after the sale, but I will tell you that dealing with troubled sellers increases the odds. Assuming the seller accepted $150,000 cash from my brother, let’s take a peek at the deal when all the smoke clears. First, my property is free ‘n clear and my cash flow has increased $1,500 per month. Also, it sorta feels like I really purchased the property for $180,000 instead of $330,000. Even if I had to borrow $150,000 cash to pay the seller for his note, I can use part of my additional cash flow to pay back the loan.

At the beginning I told you, investing is about income and profits. As you can see from my example, private financing can open the door to brand new profit opportunities for investors willing to learn and develop this technique. I have barely scratched the surface here when it comes to the many different ways you can speed up your wealth with private seller financing. My books; “THE REAL ESTATE FISHERMAN” and “INVESTING IN FIXER-UPPERS” show you a variety of different ways to increase profits with seller financing, including soliciting private note holders using my special “Christmas Letter”.

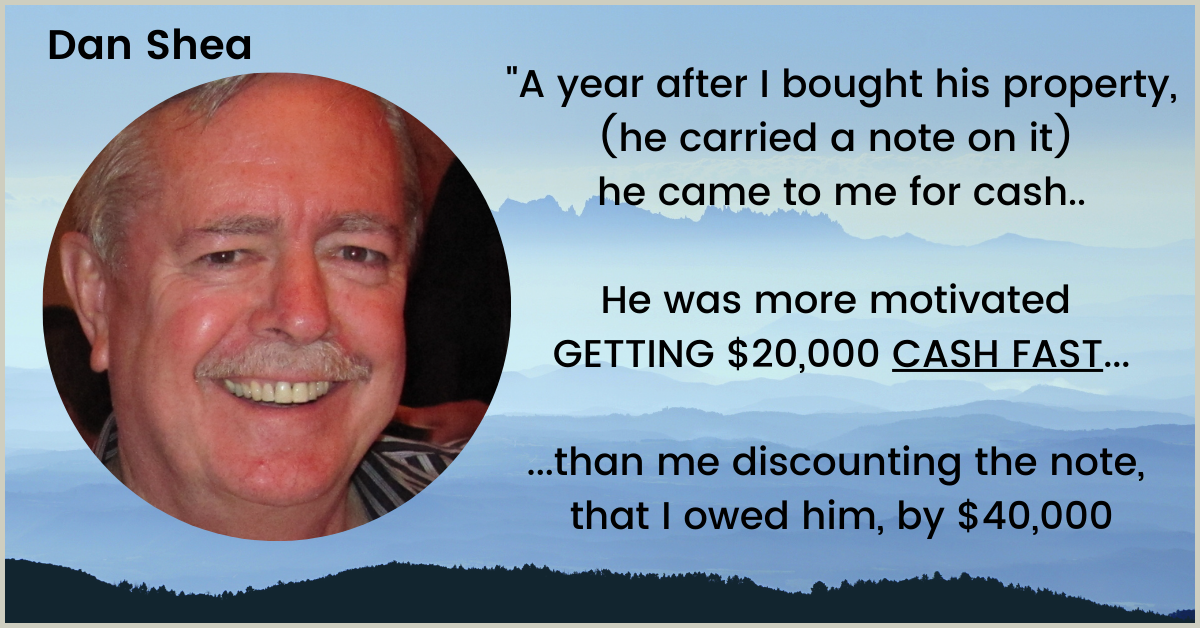

My seminar assistant and long time student Mr. Dan, developed a highly profitable technique with his seller who carried back private financing on the sale.

Almost immediately after the sale, the seller began asking Dan for money. Seems he didn’t wish to sell the note, but merely wanted a cash advance – and not just once but on multiple occasions. Dan accommodated the seller by making the note work like a line of credit. Each time the seller came back for cash, he agreed to reduce his note balance twice the amount. For example, when he asked Dan for $20,000, he reduced the note balance $40,000. Dan won’t even look at property anymore without seller financing. You can read more about Dan’s strategies in Jay’s latest book “SWEAT EQUITY”.