Defer Portion of Purchase Price (Shelving Equity)

Negative cash flow can sink your chances of becoming wealthy in real estate!

Quite often you’ll find yourself running the numbers on an income-producing property only to find that you’re light years away from having cash flow even after paying a reasonable down payment. Most likely the seller is asking too much for his property and it’s almost certain he’ll have difficulty finding a buyer. Remember now, I’m not talking about his home (personal residence) where emotions will sometimes influence his asking price. I’m talkin’ about plain ol’ income-producing real estate where pricing and value are nearly always determined by the amount of income generated. Still, if the seller’s motivation is only lukewarm and he proves to be inflexible, most interested investors will simply just walk away. By the way, that’s exactly what I would do --- unless of course…

Unless of course what - you’re no doubt wondering! Allow me to explain! There are certain situations where it’s possible to turn an over-priced property into a solid money-maker transaction using a creative technique I call equity shelving. In plain ol’ English I can do this by deferring a portion of the purchase price to some later date. Shelving tends to work best with greedy sellers on over-priced properties who won’t budge one nickel on their selling price! Often these sellers are so engrossed with their selling price (perhaps even bragging rights), yet they might be open to your creative terms.

Underline the next 29 words! You must never forget that real estate investing is a people business! Both price and terms are always subjective. My goals and values can be very different from yours. These words can be very valuable in your future negotiations.

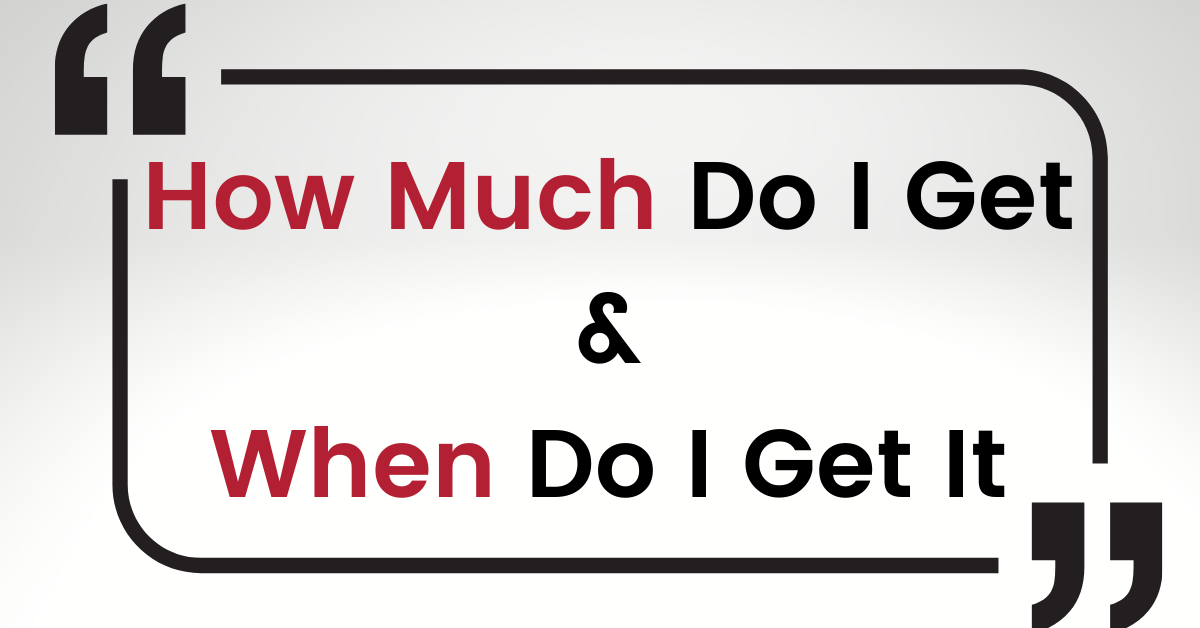

Almost any real estate transaction, buying or selling, is based on how much do I get and when do I get it. Theoretically, almost any real estate transaction can work if one party is allowed to choose how much while the other party gets to say when. As I told you above, some sellers for whatever reason become totally obsessed with their selling price and hitting them with a sledge hammer won’t get ‘em to budge. Rather than walk away, assuming you would like to own the property of course, allow me to suggest my equity shelving offer.

In the rental or leasing business, you must always remember the property is of little value to you unless your tenants can pay all the bills, both expenses and debt service (the mortgage payments). It’s your job as a negotiator to design your deals to make this possible. Average expenses for income (rental) properties are roughly 40 to 45% of the gross income. This means 55 to 60% is what’s left to service debt. I have found it’s very risky if you exceed these numbers – therefore we’ll use them in my following example of shelving equity.

INCOME PROPERTY PURCHASE PRICE $500,000

Down Payment (10%) 50,000

Balance to Finance (Mortgage Debt) 450,000

Monthly Income $5000 (100%)

Monthly Expenses 2250 (45%)

I propose to create 2 separate promissory notes – Mortgages 1 & 2.

Mortgage #1 (Seller Financing)

Monthly Payment starts now $2750 ( 55%) $350,000

Mortgage #2 (Seller Financing)

Monthly Payment Deferred $ 750 …………$100,000 Shelved Equity

As you can see the current monthly income will not support a debt service (mortgage payments) higher than $2750. Added to the expenses of $2250, it will require a total monthly payout of $5000 or 100% of the total income. Obviously as a do-it-yourself owner, a portion of the monthly expenses such as management, maintenance and repairs (15to 20%) will be mine to keep since I’ll perform those tasks myself.

I like this property very much. It’s located well near a large city college that continues to grow! The only drawback is the seller is demanding a higher price than the current rents will support. In my judgement, the price would be about right in five (5) years from now after several rounds of rent increases. The seller won’t compromise on either the sales price or mortgage payments.

It’s very clear; he has chosen to set the purchase price and payments. I can accept the deal if he’ll allow me to choose when. The following represents my delayed payment terms.

SHELVING EQUITY TERMS

Mortgage #2 – Amount of Sales Price Deferred (Shelved) …….. $100,000

- Mortgage payments ($750) per month to begin

5 years from closing date of sale.

OR …

- Mortgage payment ($750) per month shall begin

when rental income reaches ($6,000) per month.

OR

- Mortgage #2 to be paid in full if property is sold.

In my opinion, this property is an excellent long-term investment (a keeper property). I am willing to pay out the total amount of income (100%) to begin with, but not a nickel more! Part of the seller’s equity ($100,000) must be deferred or paid later when the property cranks out more income.

Rent increases during the first 5 years will provide cash flow for me. I project that modest (5%) annual rent increases will add an additional $1000 monthly income by the end of year (4). If my projection is a bit shy, I’ll still have another year before the deferred mortgage payment of ($750) kicks in!

From the seller’s perspective, he’s sold me his over-priced property at the full (100%) asking price along with the mortgage payments he asked for. His only downside is having to wait for up to five years to receive roughly 20% of his money. Even so, provisions in my terms could possible shorten his wait.

No matter how you view this hypothetical transaction – whether you believe it would work or not. Let me remind you once again of those 29 words I ask you to underline. The key words: Both price and terms are always subjective in this business. Can ya shout “Amen” like ya mean it!